Synopsis: An initial look at the impact on businesses and their owners of the reform of dividends announced in the Summer Budget.

In his Budget speech, the Chancellor said ‘Those who either pay themselves in dividends or have large shareholdings worth typically over £140,000 will pay more tax’. This was the only clue to why Mr Osborne had undertaken such a radical reform of dividends, seemingly giving away money to 85% of dividend recipients.

As we noted in our earlier Bulletins, the £5,000 dividend allowance will mean:

· Basic rate taxpayers are only worse off when their dividend income exceeds £5,000;

· Higher rate taxpayers are better off until their dividend income exceeds £21,667; and

· Additional rate taxpayers are better off until their dividend income exceeds £25,250.

The main groups who will be hit by the reforms will thus be those people with substantial investment portfolios or, more likely, who operate via private companies and draw large dividends. Such dividends will often be in lieu of salary, but they may also represent withdrawal of corporately-sheltered investment income, e.g. by individuals who use companies to hold buy-to-let portfolios (coincidentally also side stepping the new interest relief rules).

The impact of the changes on those who use dividends instead of salary or bonus (and are not caught by IR35) can be seen in the following examples.

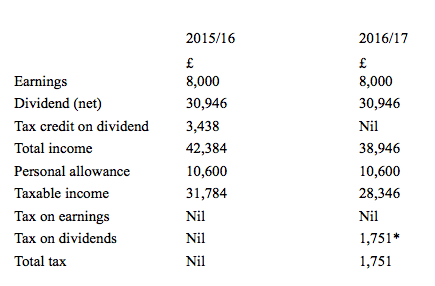

Example 1 The Typical Contractor

Peter is a contractor who operates via PeterCon Ltd. He takes just enough income to avoid reaching higher rate. He has a salary of £8,000 – just enough to avoid NICs – and draws net dividends of £30,946. Ignoring the personal allowance and tax band changes, this is what the Budget has done to Peter:

* As Peter has £2,600 of unused personal allowance once he has taken his salary, he does not start paying 7.5% tax on his dividends until they exceed £7,600.

The absence of grossing up of the dividends means that in 2016/17 Peter could draw another £3,439 of net dividends before hitting the higher rate threshold (in 2015/16 terms – the threshold will actually be £43,000 in 2016/17). If he does so he would pay another £258 in tax (£3,439 @ 7.5%). If he drew the same £3,439 extra in 2015/16 he would have a tax bill of £860 (£3,439/0.9 @ 22.5%).

Once Peter hits higher rate, every £100 of dividends is worth £75 after higher rate tax in 2015/16, but only £67.50 in 2016/17, reflecting the effective 7.5% tax rate increase.